战略系统审计资料(英文版)djgk

战略系统审计资料(英文版)djgk

《战略系统审计资料(英文版)djgk》由会员分享,可在线阅读,更多相关《战略系统审计资料(英文版)djgk(25页珍藏版)》请在装配图网上搜索。

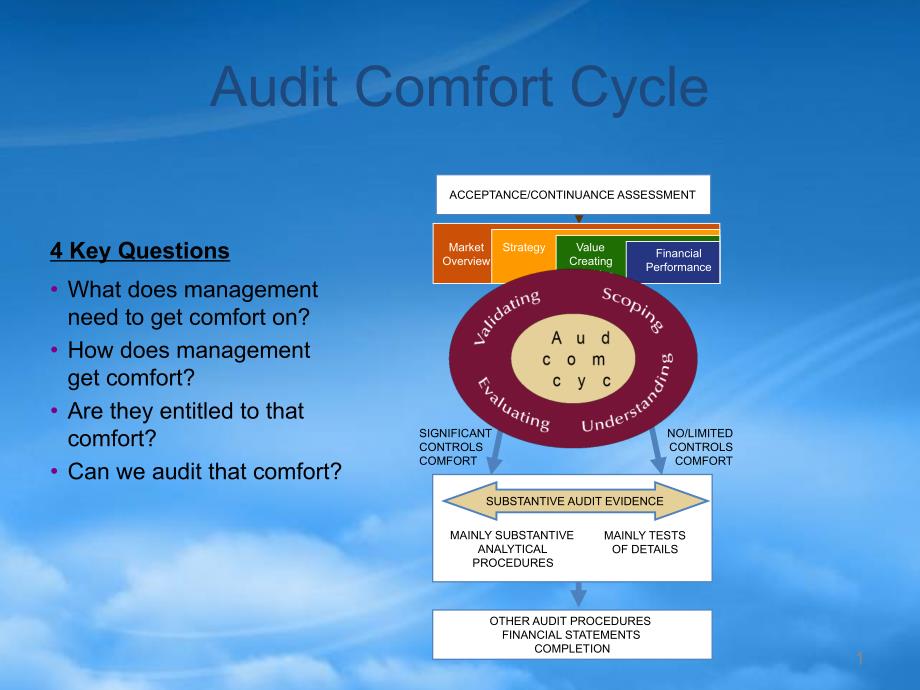

1、单击此处编辑母版标题样式,单击此处编辑母版文本样式,第二级,第三级,第四级,第五级,2021/2/8,,‹#›,Audit Comfort Cycle,4 Key Questions,What does management need to get comfort on?,How does management get comfort?,Are they entitled to that comfort?,Can we audit that comfort?,Market,,Overview,,Strategy,Value,,Creating,

2、,Activities,Financial,,Performance,OTHER AUDIT PROCEDURES,FINANCIAL STATEMENTS,COMPLETION,ACCEPTANCE/CONTINUANCE ASSESSMENT,SUBSTANTIVE AUDIT EVIDENCE,MAINLY SUBSTANTIVE,ANALYTICAL PROCEDURES,SIGNIFICANT,CONTROLS,COMFORT,NO/LIMITED,CONTROLS,COMFORT,,MAINLY TESTS OF DETAILS,1,Scoping: Forming a Poin

3、t of View,Perform company and industry analytical procedures,Research and analyze external communications,Partners connect with staff members,Document the team’s understanding of the business,Knowledge broker to capture and share industry information,Form a point of view on the risks that management

4、 should be concerned about,2,Scoping: Business Analysis Framework,3,4,Strategic Analysis,Understand the client’s strategic advantage,,5,6,7,Risk Assessment,,Understand the risks that threaten attainment of the client’s business objectives,“The primary goal of management control is to ensure that

5、risk monitoring and control activities are aligned properly with overall strategic objectives” p. 35,Strategic risks,Process risks,,8,Scoping: Risk Assessment – Key Risks,,Key Risk,We identify audit risk through understanding the entity’s business objectives and related risks.,Business Risks,Audit

6、 Risks,,Key Risk,,Key Risk,,Key Risk,,Key Risk,Key risks are those,conditions or factors within an audit that, in the judgment of the auditor, give rise to a greater risk of material financial misstatement or other matters resulting in the issuance of an inappropriate audit report.,,9,Scoping: Analy

7、tical Procedures,High Level,Understand the business,Identify areas of risk,Disaggregated Account Level,Determine the nature, timing & extent of testing,External benchmarking to peers, market trends,Looking for anomalies, areas of risk,Use of extensive knowledge management tools available,10,Business

8、 Process Analysis,Understand the key processes and related competencies needed to realize strategic advantage,Process driven competition,Measure and benchmark process performance,Document understanding of the client’s ability to create value and generate future cash flows using a client business mod

9、el, process analyses, key performance indicators, and a business risk profile,,11,Business,Risks related to achieving Objectives,……,……,……,Business Process A,Completeness,Accuracy,Validity,Restricted Access,Business Process B,Completeness,Accuracy,Validity,Restricted Access,Business Process C,Complet

10、eness,Accuracy,Validity,Restricted Access,Account Balances and Transactions,Account Balances and Transactions,General Computer Controls,Account Balances and Transactions,Connecting the Dots …,Business Objectives,Financial Statement Assertions/ Audit Objectives,,Classes of Transactions,Occurrence,Com

11、pleteness,Accuracy,Cutoff,Classification,Account Balances,Rights & Obligations,Existence,Completeness,Accuracy/Valuation,Presentation & Disclosure,Occurrence/R&O,Completeness,Understandability,Accuracy/Valuation,12,13,Assess implications for business and audit,Is risk identification complete?,Are th

12、ey prioritized properly?,Are there controls to minimize risks to acceptable level?,Do accounting choices and disclosures adequately reflect uncontrolled risks?,Groups residual business risk by financial statement assertion,,14,Scoping Translated into Audit Strategy,Where controls over significant ac

13、count balances or classes of transaction are not aligned, we will need to perform substantive tests of details.,,Stakeholders,Risks,Controls,Alignment,Business Objectives,15,Business Measurement,Use the comprehensive business knowledge decision frame to develop expectations about key assertions embo

14、died in the overall financial statements,Compare reported financial result to expectations and design additional audit test work to address any gaps between expectations and reported results,Transaction based auditing procedures are applied to non-routine transactions and non-routine and highly judg

15、mental accounting estimates (p. 36).,Computer audit techniques filter routine transactions for unusual items,Additional test work is performed when interrelated financial and Nonfinancial performance measures are inconsistent and when key financial-statement assertions are not consistent with the au

16、ditor’s understanding of the organization’s strategic-systems dynamic,Quality of earnings are assessed,Process performance evaluated on,Cycle time,Process quality,Process cost,,16,Scoping: Audit Team of Specialists,Our best teams use our specialist capabilities to help in,forming a point of view,.,S

17、takeholders,Business Objectives,Financial Risk,Business Process,Enterprise-wide Risk,Systems & Technology,Energy Trading Risk,Business Resilience,Project Management,Internal Audit,Security,Data Risk,Regulatory/ Compliance,Performance Improvement,Treasury,Risks,Controls,Alignment,Computer-Assisted Au

18、dit Techniques,Fraud,17,Audit Comfort Cycle,4 Key Questions,What does management need to get comfort on?,Market,,Overview,,Strategy,Value,,Creating,,Activities,Financial,,Performance,OTHER AUDIT PROCEDURES,FINANCIAL STATEMENTS,COMPLETION,ACCEPTANCE/CONTINUANCE ASSESSMENT,SUBSTANTIVE AUDIT EVIDENCE,M

19、AINLY SUBSTANTIVE,ANALYTICAL PROCEDURES,SIGNIFICANT,CONTROLS,COMFORT,NO/LIMITED,CONTROLS,COMFORT,,MAINLY TESTS OF DETAILS,How does management get comfort?,Are they entitled to that comfort?,Can we audit that comfort?,18,“Taking Stock”: Real-Time Linkage in the Iterative Process,Share team members’ c

20、umulative knowledge,Update risk identification and assessment,Consider the audit comfort gained to date, by audit assertion,Answer: “Do we have enough comfort?”,Answer: “What do we do next?”,,19,Substantive Audit Evidence,Market,,Overview,,Strategy,Value,,Creating,,Activities,Financial,,Performanc

21、e,OTHER AUDIT PROCEDURES,FINANCIAL STATEMENTS,COMPLETION,ACCEPTANCE/CONTINUANCE ASSESSMENT,SUBSTANTIVE AUDIT EVIDENCE,MAINLY SUBSTANTIVE,ANALYTICAL PROCEDURES,SIGNIFICANT,CONTROLS,COMFORT,NO/LIMITED,CONTROLS,COMFORT,,MAINLY TESTS OF DETAILS,20,Assurance Hierarchy,Will we obtain audit assurance from

22、tests of controls?,Test controls.,No further testing required.,Can we obtain audit assurance from substantive analytical procedures?,Perform substantive analytical procedures.,Perform tests of details.,Do we need additional audit assurance?,No,Yes,No,No,Yes,Yes,21,Other Audit Procedures,Market,,Over

23、view,,Strategy,Value,,Creating,,Activities,Financial,,Performance,OTHER AUDIT PROCEDURES,FINANCIAL STATEMENTS,COMPLETION,ACCEPTANCE/CONTINUANCE ASSESSMENT,SUBSTANTIVE AUDIT EVIDENCE,MAINLY SUBSTANTIVE,ANALYTICAL PROCEDURES,SIGNIFICANT,CONTROLS,COMFORT,NO/LIMITED,CONTROLS,COMFORT,,MAINLY TESTS OF DET

24、AILS,22,Other Audit Procedures: More Connecting the Dots,Link,management information,to financial statements,Review,adjustments,necessary to reconcile management information to the financial statements,Review non-standard journal entries and other adjustments to ascertain whether entries may be,indicative of fraud,based upon the risk of management override on controls,Perform ongoing analytical procedures, including updating,analytical procedures,related to revenue,,23,Continuous Improvement,,Feedback to capital suppliers and inside process owners,,24,

- 温馨提示:

1: 本站所有资源如无特殊说明,都需要本地电脑安装OFFICE2007和PDF阅读器。图纸软件为CAD,CAXA,PROE,UG,SolidWorks等.压缩文件请下载最新的WinRAR软件解压。

2: 本站的文档不包含任何第三方提供的附件图纸等,如果需要附件,请联系上传者。文件的所有权益归上传用户所有。

3.本站RAR压缩包中若带图纸,网页内容里面会有图纸预览,若没有图纸预览就没有图纸。

4. 未经权益所有人同意不得将文件中的内容挪作商业或盈利用途。

5. 装配图网仅提供信息存储空间,仅对用户上传内容的表现方式做保护处理,对用户上传分享的文档内容本身不做任何修改或编辑,并不能对任何下载内容负责。

6. 下载文件中如有侵权或不适当内容,请与我们联系,我们立即纠正。

7. 本站不保证下载资源的准确性、安全性和完整性, 同时也不承担用户因使用这些下载资源对自己和他人造成任何形式的伤害或损失。